Lots of Capital = Less Attractive Returns

Ultimately the best investment managers will tend to have between $1-50 Billion under management or less (with long term average results of at least 15% after fees and expenses). That is because as you get beyond managing an amount greater than $50 Billion you have serious limitations insofar as your "investment universe" is concerned. To illustrate, say capital under management is indeed $50 Billion.

Lets assume two different managers, (i) and (ii). (i) owns 100 different companies and (ii) owns only 20-both are fully invested. With no other limitations (i) would be limited to businesses available for $500 million and above and (ii) limited to $2.5 Billion and above. But this is unrealistic since almost every fund of has some restriction as to the amount of ownership which can be established in any single business. Therefore assume limits of 25% and 5% ownership.

Now (i) is limited to

@25%, 500 Million x 4 = $2 Billion

@ 5%, 500 Million x 20 = $10 Billion

And (ii) limited to:

@25%, 2.5 Billion x 4 = $10 Billion

@ 5%, 2.5 Billion x 20 = $50 Billion

According to Morningstar, Total universe = 8831 stocks:

Businesses with market capitalizations greater than or equal to:

Market Cap.................. number of businesses

$ 0.5 Billion.................... 2666

$ 2.0 Billion..................... 1429

$ 2.5 Billion .................... 1291

$ 3.0 Billion ...................... 1137

$ 5.0 Billion ........................ 827

$10.0 Billion .....................526

$20.0 Billion ........................322

$50.0 Billion ......................131

Oh but now for a bit of reality. Lets make this realistic and say I am interested in only those funds that provide investors with long-term attractive rates of return or at least better returns than offered by an index fund after fees and expenses. So lets assume 10% as a better than average return, which it is or isn't depending on the period of years. Let's do a simple case, those businesses that meet the foregoing Market Cap restrictions, and earned 10% return on equity for the previous year (which I actually consider very average). This will obviously overstate the realistic number were we to look at only those with moderate amounts of leverage and who earned a 10 year return on equity at or above 10% and not just for a single year. At any rate:

The number of companies, Market Cap & 10%+ Return on equity

Market Cap................... number of businesses

$ 0.5 Billion................. 1651

$ 2.5 Billion.................. 950

$10.0 Billion................. 436

$50.0 Billion.................. 116

This is a long winded way of making the point that as you get above $50 Billion of investment Capital you quickly become restricted as to where one might intelligibly allocate investment capital. Oh, the number of businesses above $50 billion and earn at least 20% return on Equity (single year) amount to only 71 businesses, not removing therefrom those that are very highly leveraged.

A very, very limited list of such really, really great Investment Funds: (No Order)

Fund name, (State) Primary Manager

Fairholme (recently moved to Miami from NY) Bruce Berkowitz

Baupost Group (Boston) Seth Klarman

First Manhattan Consulting Group (NY) Sandy Gottesman

Gotham Capital (NY) Joel Greenblatt

Weiss Asset Management (Boston) Andrew Weiss

Tweedy Browne (New York) Christopher Browne

Chieftain Capital (NY) Glenn Greenburg

Longleaf Partners (Tennessee) Mason Hawkins

Semper Vic, under Gardner Russo & Gardner (PA) Tom Russo

Markel-Asset Management (Virginia) Thomas Gayner

H.L. Lichstrahl & Company (Virginia) Howard Lichstrahl

Lets assume two different managers, (i) and (ii). (i) owns 100 different companies and (ii) owns only 20-both are fully invested. With no other limitations (i) would be limited to businesses available for $500 million and above and (ii) limited to $2.5 Billion and above. But this is unrealistic since almost every fund of has some restriction as to the amount of ownership which can be established in any single business. Therefore assume limits of 25% and 5% ownership.

Now (i) is limited to

@25%, 500 Million x 4 = $2 Billion

@ 5%, 500 Million x 20 = $10 Billion

And (ii) limited to:

@25%, 2.5 Billion x 4 = $10 Billion

@ 5%, 2.5 Billion x 20 = $50 Billion

According to Morningstar, Total universe = 8831 stocks:

Businesses with market capitalizations greater than or equal to:

Market Cap.................. number of businesses

$ 0.5 Billion.................... 2666

$ 2.0 Billion..................... 1429

$ 2.5 Billion .................... 1291

$ 3.0 Billion ...................... 1137

$ 5.0 Billion ........................ 827

$10.0 Billion .....................526

$20.0 Billion ........................322

$50.0 Billion ......................131

Oh but now for a bit of reality. Lets make this realistic and say I am interested in only those funds that provide investors with long-term attractive rates of return or at least better returns than offered by an index fund after fees and expenses. So lets assume 10% as a better than average return, which it is or isn't depending on the period of years. Let's do a simple case, those businesses that meet the foregoing Market Cap restrictions, and earned 10% return on equity for the previous year (which I actually consider very average). This will obviously overstate the realistic number were we to look at only those with moderate amounts of leverage and who earned a 10 year return on equity at or above 10% and not just for a single year. At any rate:

The number of companies, Market Cap & 10%+ Return on equity

Market Cap................... number of businesses

$ 0.5 Billion................. 1651

$ 2.5 Billion.................. 950

$10.0 Billion................. 436

$50.0 Billion.................. 116

This is a long winded way of making the point that as you get above $50 Billion of investment Capital you quickly become restricted as to where one might intelligibly allocate investment capital. Oh, the number of businesses above $50 billion and earn at least 20% return on Equity (single year) amount to only 71 businesses, not removing therefrom those that are very highly leveraged.

A very, very limited list of such really, really great Investment Funds: (No Order)

Fund name, (State) Primary Manager

Fairholme (recently moved to Miami from NY) Bruce Berkowitz

Baupost Group (Boston) Seth Klarman

First Manhattan Consulting Group (NY) Sandy Gottesman

Gotham Capital (NY) Joel Greenblatt

Weiss Asset Management (Boston) Andrew Weiss

Tweedy Browne (New York) Christopher Browne

Chieftain Capital (NY) Glenn Greenburg

Longleaf Partners (Tennessee) Mason Hawkins

Semper Vic, under Gardner Russo & Gardner (PA) Tom Russo

Markel-Asset Management (Virginia) Thomas Gayner

H.L. Lichstrahl & Company (Virginia) Howard Lichstrahl

Better understanding of investments, Diversification, Books, The Economy...

Books:

You should be very careful what you read and who wrote it. You want to keep the noise to a minimum.

Read and re-read intelligent investor. May be boring but you need to understand what he says in that book.

Then go read The little book on value investing. By Christopher Browne. There is a lot of good additional material on his funds site, tweedybrowne.com

Before getting into Security Anaysis (1940 best to begin with) I would become familiar with what some accounting:

Tutorial on Financial Statements:

http://www.baruch.cuny.edu/tutorials/statements/

As you are learning try to think about the following: what is the company really earning and what can they expect to earn in the future? Also what do you reasonably not know?

Diversification?

Diversification is over used. The typical issue with investing in only a few businesses is that aggregate returns could be adversely affected by any one security. Investment selection should be based upon a thorough

understanding of each business and its underlying economics, acquired only at sensible prices. While seemingly obvious, the fact is that most people who buy fractional ownership do not know nearly what they should to make informed long-term investment decisions (the so called "professionals" included).

Ultimately, the premise is that it makes more sense to invest large amounts in those businesses with which you understand a great deal, instead of putting very small amounts in many business that you understand very little. Concentration may very well decrease risk if it raises, as it should, both the intensity with which an investor thinks about a business and the comfort-level he must feel with its economic characteristics before buying an ownership interest.

Some stuff to think about:

The fundamental purpose to save or invest versus spend is to have more money in the future. In a simple world, one without inflation or investments as alternatives to saving, the money grows through saving more out of income relative to what is consumed, or spent. Today’s dollars are valued in the same terms as are tomorrow’s dollars. Any interest earned on savings translates into increased purchasing power-the ability to buy something.

Introduce Inflation and money not spent must earn an amount equal to the inflation rate just to maintain purchasing power. This is because $1 today with 3% inflation means that you need $1.03 in a year from now in order to have the same "purchasing power". That is what costs $1 today costs $1.03 next year, so if you save (or invest) you must earn at least 3%, otherwise you have less money than you started with. If you are unable to earn 3% you should just spend the money.

In this world the fundamental problem is where to put money in order to grow future purchasing power. This implies a reasonable rate of return over inflation (ignoring income taxes for now).

On the Economy:

A few things on the economy and the "markets". Don't worry about what people say, friends, media, whoever. In the last 100 years we have had two world wars, a great depression where unemployment reached unbelievable levels, two almost three serious financial fiascos, 9-11, the cold war, an assassinated president, etc. yet our living standards increased seven-fold. So called "bad-times" lead to good investment opportunities because of depressed prices, but only those who didn't loose money are able to take advantage of this. I'll spare you, with more details. The moral being do not pay attention to discussions about interest rates, the economy, the stock market, etc. do what makes sense at all times, nothing less.

I hate thinking of business valuations like this but you may come across such terms and should be familiar with them:

Generally speaking, there are two very broad and contrasting ideas: a “macro” perspective as opposed to a "micro" perspective. A macro approach is often also called a “top down approach” whereas micro is bottom up. Basically the macro approach looks at things like sectors or industries, potential changes in interest rates, foreign exchange rates, and the like. For more information on the differences between top down and bottom up see the following link:

http://www.tiaa-cref.org/about/press/publications/market_monitor/2006_11_20.

pdf

It takes time and effort!

If investing were easy to do there would be many, many more people like Warren Buffet. And while there are many people that have made great fortunes in the investment management and related businesses nearly all of them made their money on fees not associated with actual investment results. So this is one reason not to pay attention to about 99% of these guys especially those on TV. Of the investors who actually invest in securities with successful long term “track records” nearly all of them might be referred to as Value Investors, with the exception of maybe one. George Soros is a successful investor who practices what seems to be a very much top down approach, but the problem is that he cannot explain his success although others will claim that they can. Some have written books about his approach, but if they truly understood it they would apply it by investing and not so much by writing books. (Same goes for all those books on Buffett.)

It is not my intent to undermine investors like Soros, but his approach or selection process is almost equivalent to throwing darts (at least as far as outsiders are concerned). For one, it is truly difficult to determine what

the ultimate factors were in their decision making process.

Assume one makes a decision to buy a given stock, the stock price goes up, and then the person decided to sell at a profit. Can it be said that a good investment decision has been made?

This has a very dangerous implication too often overlooked. Just because you made money on an investment doesn’t necessarily make it a good decision. If you invested in a housing company and a year later you sell making a 20% return on your investment you might conclude that indeed your choice was a good one in which case you are likely to make future investments based upon a similar thought process. But if the reason you decided to invest in that company was made based upon a belief that demand for new housing was to increase in the near term, but the company decided that demand for new houses was actually declining and in response they issued a regular dividend that appealed to the big mutual funds resulting in the biding up of the stock price.

Such would not qualify as a good investment decision in my mind, because the next investment

is not likely to result in such a positive outcome. That is, the next company you invest in may not have funds to distribute as a dividend and the price may very well then drop off significantly-the direct result of failing to account for price paid relative to reasonable business value.

"You are correct only because your decision was based on the facts and sound logic."

The Term Value Investing:

By the way The term Value investor is redundant. Value investing is considered purchasing businesses for less than they would sell to a knowledgeable buyer in a negotiated transaction. But this is the only form

of an "investment", otherwise you are speculating. Furthermore, the purchase of commons stocks must always be thought of as buying fractional ownership of the entire business. So think of "Value Investing" simply as "investing" and everything else as speculating. Speculating is the purchase of a "stock" on the basis that you believe the stock price will go up. Speculators in other words, DO NOT ask themselves (i) what exactly am I buying and (ii) is the price being offered an attractive one?

You should be very careful what you read and who wrote it. You want to keep the noise to a minimum.

Read and re-read intelligent investor. May be boring but you need to understand what he says in that book.

Then go read The little book on value investing. By Christopher Browne. There is a lot of good additional material on his funds site, tweedybrowne.com

Before getting into Security Anaysis (1940 best to begin with) I would become familiar with what some accounting:

Tutorial on Financial Statements:

http://www.baruch.cuny.edu/tutorials/statements/

As you are learning try to think about the following: what is the company really earning and what can they expect to earn in the future? Also what do you reasonably not know?

Diversification?

Diversification is over used. The typical issue with investing in only a few businesses is that aggregate returns could be adversely affected by any one security. Investment selection should be based upon a thorough

understanding of each business and its underlying economics, acquired only at sensible prices. While seemingly obvious, the fact is that most people who buy fractional ownership do not know nearly what they should to make informed long-term investment decisions (the so called "professionals" included).

Ultimately, the premise is that it makes more sense to invest large amounts in those businesses with which you understand a great deal, instead of putting very small amounts in many business that you understand very little. Concentration may very well decrease risk if it raises, as it should, both the intensity with which an investor thinks about a business and the comfort-level he must feel with its economic characteristics before buying an ownership interest.

Some stuff to think about:

The fundamental purpose to save or invest versus spend is to have more money in the future. In a simple world, one without inflation or investments as alternatives to saving, the money grows through saving more out of income relative to what is consumed, or spent. Today’s dollars are valued in the same terms as are tomorrow’s dollars. Any interest earned on savings translates into increased purchasing power-the ability to buy something.

Introduce Inflation and money not spent must earn an amount equal to the inflation rate just to maintain purchasing power. This is because $1 today with 3% inflation means that you need $1.03 in a year from now in order to have the same "purchasing power". That is what costs $1 today costs $1.03 next year, so if you save (or invest) you must earn at least 3%, otherwise you have less money than you started with. If you are unable to earn 3% you should just spend the money.

In this world the fundamental problem is where to put money in order to grow future purchasing power. This implies a reasonable rate of return over inflation (ignoring income taxes for now).

On the Economy:

A few things on the economy and the "markets". Don't worry about what people say, friends, media, whoever. In the last 100 years we have had two world wars, a great depression where unemployment reached unbelievable levels, two almost three serious financial fiascos, 9-11, the cold war, an assassinated president, etc. yet our living standards increased seven-fold. So called "bad-times" lead to good investment opportunities because of depressed prices, but only those who didn't loose money are able to take advantage of this. I'll spare you, with more details. The moral being do not pay attention to discussions about interest rates, the economy, the stock market, etc. do what makes sense at all times, nothing less.

I hate thinking of business valuations like this but you may come across such terms and should be familiar with them:

Generally speaking, there are two very broad and contrasting ideas: a “macro” perspective as opposed to a "micro" perspective. A macro approach is often also called a “top down approach” whereas micro is bottom up. Basically the macro approach looks at things like sectors or industries, potential changes in interest rates, foreign exchange rates, and the like. For more information on the differences between top down and bottom up see the following link:

http://www.tiaa-cref.org/about/press/publications/market_monitor/2006_11_20.

It takes time and effort!

If investing were easy to do there would be many, many more people like Warren Buffet. And while there are many people that have made great fortunes in the investment management and related businesses nearly all of them made their money on fees not associated with actual investment results. So this is one reason not to pay attention to about 99% of these guys especially those on TV. Of the investors who actually invest in securities with successful long term “track records” nearly all of them might be referred to as Value Investors, with the exception of maybe one. George Soros is a successful investor who practices what seems to be a very much top down approach, but the problem is that he cannot explain his success although others will claim that they can. Some have written books about his approach, but if they truly understood it they would apply it by investing and not so much by writing books. (Same goes for all those books on Buffett.)

It is not my intent to undermine investors like Soros, but his approach or selection process is almost equivalent to throwing darts (at least as far as outsiders are concerned). For one, it is truly difficult to determine what

the ultimate factors were in their decision making process.

Assume one makes a decision to buy a given stock, the stock price goes up, and then the person decided to sell at a profit. Can it be said that a good investment decision has been made?

This has a very dangerous implication too often overlooked. Just because you made money on an investment doesn’t necessarily make it a good decision. If you invested in a housing company and a year later you sell making a 20% return on your investment you might conclude that indeed your choice was a good one in which case you are likely to make future investments based upon a similar thought process. But if the reason you decided to invest in that company was made based upon a belief that demand for new housing was to increase in the near term, but the company decided that demand for new houses was actually declining and in response they issued a regular dividend that appealed to the big mutual funds resulting in the biding up of the stock price.

Such would not qualify as a good investment decision in my mind, because the next investment

is not likely to result in such a positive outcome. That is, the next company you invest in may not have funds to distribute as a dividend and the price may very well then drop off significantly-the direct result of failing to account for price paid relative to reasonable business value.

"You are correct only because your decision was based on the facts and sound logic."

The Term Value Investing:

By the way The term Value investor is redundant. Value investing is considered purchasing businesses for less than they would sell to a knowledgeable buyer in a negotiated transaction. But this is the only form

of an "investment", otherwise you are speculating. Furthermore, the purchase of commons stocks must always be thought of as buying fractional ownership of the entire business. So think of "Value Investing" simply as "investing" and everything else as speculating. Speculating is the purchase of a "stock" on the basis that you believe the stock price will go up. Speculators in other words, DO NOT ask themselves (i) what exactly am I buying and (ii) is the price being offered an attractive one?

Follow up:

My friend has Pioneer. They are worse.

I told him that his returns were 80% of the returns Pioneer claims to earn.

He asked, "So are you saying that Pioneer's fees are 20%"?

My Response:

No, well not really: Industry standard is that charges are a % of assets, but they can increase assets more and more as people give them money through 401k's etc. The other factor is the "load" either front-end or back, both are bad. What matters to you however is how much of the money that you "earned" (the amount in excess of the amount that you directly put in), will you actually be able to take away. In other words there is what they call a "total return", (what the fund claims to have "earned" you) and then there is the amount that you can put in the bank at the time of sale called redemption (excluding income taxes). The amount (again pre-tax) you can put in the bank is much less than the "total return". It is actually the total return less fees and expenses.

Therefore in response to, "So are you saying that pioneer's fees are 20%," the answer is no but yes. Technically they charge you something like 0.7% per year in expenses in combination with the front-load fee (4.5%? Or whatever it was) actually reduce the "total return" by 20%. So the answer is also yes your take-away return is actually 0.80 or 80% of the "total return".

Maybe an example:

You put in $10,000 and for ease, assume you never add to it. With the front load (say of 4.5%) you actually begin not with $10,000, but with $9550 because:

95.5% = (100% - 4.5%) and .955 x $10000 = 9550.

And from then on you are expensed each year at some seemingly marginal rate, but that is in essence cumulative and takes away from your take away returns as well.

So Lets assume they report to you that they earned 10% and they do this each year for 20 years. Your $10,000 should now be $67,275, which of course is an annual return of 10%.

This is a simple calculation which you could do with a constant rate of return, its just 10,000 x 1.10^20 (note ^20 is "to the 20th power")

So they can claim to have earned you 10%, but wait a minute, you began, not with $10,000, but with $9550 due to the front end load, which at 10% for 20 years would be $64,247.62

Yet there is still more since each year they are deducting the annual expense from your balance. So if for each year your funds go up by 10%, the 10% is immediately reduced by say 0.7% or 0.007. This may seem like a small number but over time this "frictional" cost is significant.

The end result is that they may claim to have earned you 10% annually, but after calculating the cumulative frictional costs and reducing the beginning balance by the front load fee, 10% is actually 10% x (1-.20) or 10% x .80 = 8%.

The result, the take away dollar amount (pre tax) from your $10,000 investment would be 46,609.57 not $67,275. Big difference! Oh and by the way, these funds WILL NOT EARN 10% ANYWAY and will be lucky to earn 8% before these expenses, but that is another discussion altogether.

My friend has Pioneer. They are worse.

I told him that his returns were 80% of the returns Pioneer claims to earn.

He asked, "So are you saying that Pioneer's fees are 20%"?

My Response:

No, well not really: Industry standard is that charges are a % of assets, but they can increase assets more and more as people give them money through 401k's etc. The other factor is the "load" either front-end or back, both are bad. What matters to you however is how much of the money that you "earned" (the amount in excess of the amount that you directly put in), will you actually be able to take away. In other words there is what they call a "total return", (what the fund claims to have "earned" you) and then there is the amount that you can put in the bank at the time of sale called redemption (excluding income taxes). The amount (again pre-tax) you can put in the bank is much less than the "total return". It is actually the total return less fees and expenses.

Therefore in response to, "So are you saying that pioneer's fees are 20%," the answer is no but yes. Technically they charge you something like 0.7% per year in expenses in combination with the front-load fee (4.5%? Or whatever it was) actually reduce the "total return" by 20%. So the answer is also yes your take-away return is actually 0.80 or 80% of the "total return".

Maybe an example:

You put in $10,000 and for ease, assume you never add to it. With the front load (say of 4.5%) you actually begin not with $10,000, but with $9550 because:

95.5% = (100% - 4.5%) and .955 x $10000 = 9550.

And from then on you are expensed each year at some seemingly marginal rate, but that is in essence cumulative and takes away from your take away returns as well.

So Lets assume they report to you that they earned 10% and they do this each year for 20 years. Your $10,000 should now be $67,275, which of course is an annual return of 10%.

This is a simple calculation which you could do with a constant rate of return, its just 10,000 x 1.10^20 (note ^20 is "to the 20th power")

So they can claim to have earned you 10%, but wait a minute, you began, not with $10,000, but with $9550 due to the front end load, which at 10% for 20 years would be $64,247.62

Yet there is still more since each year they are deducting the annual expense from your balance. So if for each year your funds go up by 10%, the 10% is immediately reduced by say 0.7% or 0.007. This may seem like a small number but over time this "frictional" cost is significant.

The end result is that they may claim to have earned you 10% annually, but after calculating the cumulative frictional costs and reducing the beginning balance by the front load fee, 10% is actually 10% x (1-.20) or 10% x .80 = 8%.

The result, the take away dollar amount (pre tax) from your $10,000 investment would be 46,609.57 not $67,275. Big difference! Oh and by the way, these funds WILL NOT EARN 10% ANYWAY and will be lucky to earn 8% before these expenses, but that is another discussion altogether.

Why Mutual Funds are not really the best option

American Funds :

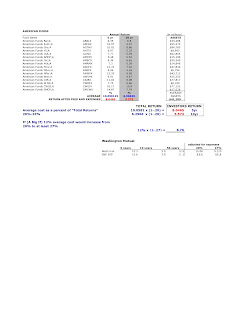

Assets under Management, 1.4 Trillion Dollars no wonder the aggregate returns are only average. Incentives are to accumulate investor funds, not to earn investors money.

Assets under Management, 1.4 Trillion Dollars no wonder the aggregate returns are only average. Incentives are to accumulate investor funds, not to earn investors money.

I am dumbfounded as to why people continue to fund institutions that provide significantly less than an index return. It is just crazy to me that (for example) American Funds with 1.4 Trillion Dollars under management, boast to investors an (aggregate) compounded annual return over the last 5 and 10 year periods of 10% and 6.9% respectively. Although only very average, is unfortunately very much overstated. After consideration of fees and expenses, these 5 & 10 year returns would be reduced to 8.14% and 5.5% respectively and that is before income (capital gains) tax. Furthermore they may claim a 12% return to investors since inception (56 years) which after fees and expenses turns out to be 8.76% versus a return for the for the S&P 500 of 11.1%. -Makes no sense to me-

{kind=link}

Assets under Management, 1.4 Trillion Dollars no wonder the aggregate returns are only average. Incentives are to accumulate investor funds, not to earn investors money.

Assets under Management, 1.4 Trillion Dollars no wonder the aggregate returns are only average. Incentives are to accumulate investor funds, not to earn investors money.I am dumbfounded as to why people continue to fund institutions that provide significantly less than an index return. It is just crazy to me that (for example) American Funds with 1.4 Trillion Dollars under management, boast to investors an (aggregate) compounded annual return over the last 5 and 10 year periods of 10% and 6.9% respectively. Although only very average, is unfortunately very much overstated. After consideration of fees and expenses, these 5 & 10 year returns would be reduced to 8.14% and 5.5% respectively and that is before income (capital gains) tax. Furthermore they may claim a 12% return to investors since inception (56 years) which after fees and expenses turns out to be 8.76% versus a return for the for the S&P 500 of 11.1%. -Makes no sense to me-

Subscribe to:

Posts (Atom)