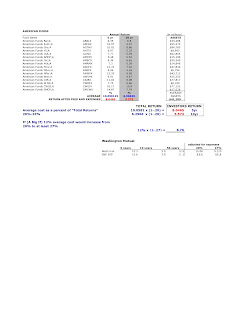

Ambassador's Group (EPAX)

The company earns on average between 30% & 40% on equity and have never really had any debt. Earnings, Sales, and CF have all grown at 17% (previous 5 years). They pay out a large portion of earnings as dividends. They have never lost money, and the lowest return on equity was 20%-though their record is only 7 years.

It's a small issue, market cap only, $158 million.

AND FOR THE KICKER: They have $100 million in muni's and cash, NO DEBT. The only Tangible assets consist of a $24 million building that is their headquarters, but it looks as though they did as lease-back.

The company is Ambassadors Group, inc.(symbol EPAX), they are in the business of providing educational travel programs for students, athletes and professionals.

A large portion of their current liabilities are in the form of "participant deposits" which are more like an unearned premium reserve, not a liability (i.e. "float").

The relatively large 2007 Capital Expenditure was for the purchase of a building that serves as their headquarters.

They also made an acquisition this year and paid out $8.7 mil in cash.

Management stated in their most recent conference call that the number of 2009 participants is (don’t remember the actual number) pretty good-but also that people can still get a refund. I expect that they will have a decrease in the number of “participants” next year though even if they were to go back to the earnings level in 2000 they would still be earning good return.

The only real issue is that last year a boy died while hiking Mt. Figi. He was diabetic. The family is suing for wrongful death and the trial will take place in late 2009. Based upon what I know about tort law, which is certainly limited, I don’t see how the company would be liable for more than a few million-which would be fine. The only question is how this will affect their image-so far it hasn’t.

As of December ‘07 there where only 68 shareholders (not including management and board members). I suppose those that do follow them are concerned with the declining participant enrollment, and partly also the law suit.

What I don’t like are the option grants. Compensation is also somewhat high, but at the end of the day they have been earning very high returns for investors.

The Value of Berkshire Hathaway

11/17/08

Berkshire's insurance business is worth at least $70 billion. Berkshire has $140 billion in cash and securities, (though intrinsically worth more). Manufacturing and retail is worth at the very least, $16.5 Billion and Utilities at least $10 Billion. I left out the financial businesses and a few others because, in essence, they are free:

(In Billions of dollars) Minimum Business Value = 70+140+16.5+10 = $240 billion vs. Market Value = $150 billion a 40% discount.

The underlying business value should compound at 15% annually over 5-year periods, irrespective of the markets appraisal (and Mr. Buffett's comments at last year's meeting). Buffett has set up the business in such a way that the underlying business value will continue its compounding rate of return for generations.

Unless an investor thinks they can earn better than 15% annually, Berkshire is an attractive commitment.

Berkshire's insurance business is worth at least $70 billion. Berkshire has $140 billion in cash and securities, (though intrinsically worth more). Manufacturing and retail is worth at the very least, $16.5 Billion and Utilities at least $10 Billion. I left out the financial businesses and a few others because, in essence, they are free:

(In Billions of dollars) Minimum Business Value = 70+140+16.5+10 = $240 billion vs. Market Value = $150 billion a 40% discount.

The underlying business value should compound at 15% annually over 5-year periods, irrespective of the markets appraisal (and Mr. Buffett's comments at last year's meeting). Buffett has set up the business in such a way that the underlying business value will continue its compounding rate of return for generations.

Unless an investor thinks they can earn better than 15% annually, Berkshire is an attractive commitment.

Arbitrage anyone?

Company is Arcandor AG (German). Not a really good business, but the investment certainly appears to be.

Arcandor (Germany) a holding company that owns primarily three businesses, but you only really have to concern yourself with one. Arcandor owns owns 52% of Thomas Cook Group PLC (UK), which has lots of subsidiaries around the world. Arcandor is 54% owned by two entities: 26.4% by Madeleine Schickedanz (Forbes 142) and 28.2% by Sal. Oppenheim-a Private European Bank based in Cologne and has a direct relationship with Ms. Schickedanz.

Thomas Cook Group PLC is listed on the LSE with a market Cap of $2.389 billion. Arcandor's 52% ownership is therefore worth $1.2 billion. Arcandor is selling for $650 million, down 90% YTD mostly on concerns about its retail division, Karstadt. Looks as though they have gotten past some of the S-T borrowing issues and that the price has some asset protection from further decline. There are also some Arcandor converts out there which are exchangeable into Thomas Cook Group PLC Shares.

Though not always meaningful:

P/B is 0.64

(If I recall correctly, P/E is 0.33 ish)

Might consider Arcandor individually, or by also selling Thomas Cook TCG against it.

Discussion of liquidity issues:

http://www.forbes.com/2008/09/24/arcandor-refinancing-germany-markets-equity-cx_vr_0924markets08.html

http://www.oppenheim.de/internet/presseportal/10_pressemitteilungen/2008/2008-09-29_arcandor/2008-09-29_pr_arcandor.pdf

Also, BayernLB, Dresdner Bank AG, Royal Bank of Scotland plc all agreed to extend financing.

website is:

http://www.arcandor.com/en/index.asp

Arcandor (Germany) a holding company that owns primarily three businesses, but you only really have to concern yourself with one. Arcandor owns owns 52% of Thomas Cook Group PLC (UK), which has lots of subsidiaries around the world. Arcandor is 54% owned by two entities: 26.4% by Madeleine Schickedanz (Forbes 142) and 28.2% by Sal. Oppenheim-a Private European Bank based in Cologne and has a direct relationship with Ms. Schickedanz.

Thomas Cook Group PLC is listed on the LSE with a market Cap of $2.389 billion. Arcandor's 52% ownership is therefore worth $1.2 billion. Arcandor is selling for $650 million, down 90% YTD mostly on concerns about its retail division, Karstadt. Looks as though they have gotten past some of the S-T borrowing issues and that the price has some asset protection from further decline. There are also some Arcandor converts out there which are exchangeable into Thomas Cook Group PLC Shares.

Though not always meaningful:

P/B is 0.64

(If I recall correctly, P/E is 0.33 ish)

Might consider Arcandor individually, or by also selling Thomas Cook TCG against it.

Discussion of liquidity issues:

http://www.forbes.com/2008/09/24/arcandor-refinancing-germany-markets-equity-cx_vr_0924markets08.html

http://www.oppenheim.de/internet/presseportal/10_pressemitteilungen/2008/2008-09-29_arcandor/2008-09-29_pr_arcandor.pdf

Also, BayernLB, Dresdner Bank AG, Royal Bank of Scotland plc all agreed to extend financing.

website is:

http://www.arcandor.com/en/index.asp

Coca Cola Very Attractive OCT, 20 2008

Don't expect me to make a habit of this: Investment opportunity of the decade, COCA COLA (KO).

Coca Cola truly earns an excess of 60% on tangible assets, the result of substantial economic goodwill. (An "inflation hedge" of the purest form.)

Approximately $18-19 billion has been invested into their operating business. In 2001, Coca Cola's net worth was about $11.3 billion. Over the previous 5 years, approximately $7.657 billion of additional owner capital was reinvested into operations which provides for the foregoing $18 & $19 billion.

Owner earnings for 2007, an easy number to calculate for Coca Cola, was about $5.5 billion.

The return on total and incremental capital is about 30%. About half is paid to the owners via dividends, and the other half allocated by Coca Cola's Management (33% or so used for buybacks).

For each $1 reinvested into the operations, about $4 will result in the underlying value of the business' operations. I expect this reinvested amount (in absolute terms) to increase by 8% per annum-a result of their incredible economics. Based upon this alone the company might very well sell in a negotiated transaction today for $100 billion to a business man. (Wall street I imagine would happily pay a minimum of $150.)

Some might add $21 billion thereto to compensate for dividends. They might then justify paying somewhere between $150 & $175 billion for Coca Cola. In the end such a price might not result poorly, but it is not what I consider very attractive either.

I think a reasonable price is $115 billion, though ideally it would be bought for $100 billion. As of Friday it was selling for about $105 billion. Such an inexpensive price for an outstanding company does not offer itself very often. I strongly suggest purchases of large quantities.

Coca Cola truly earns an excess of 60% on tangible assets, the result of substantial economic goodwill. (An "inflation hedge" of the purest form.)

Approximately $18-19 billion has been invested into their operating business. In 2001, Coca Cola's net worth was about $11.3 billion. Over the previous 5 years, approximately $7.657 billion of additional owner capital was reinvested into operations which provides for the foregoing $18 & $19 billion.

Owner earnings for 2007, an easy number to calculate for Coca Cola, was about $5.5 billion.

The return on total and incremental capital is about 30%. About half is paid to the owners via dividends, and the other half allocated by Coca Cola's Management (33% or so used for buybacks).

For each $1 reinvested into the operations, about $4 will result in the underlying value of the business' operations. I expect this reinvested amount (in absolute terms) to increase by 8% per annum-a result of their incredible economics. Based upon this alone the company might very well sell in a negotiated transaction today for $100 billion to a business man. (Wall street I imagine would happily pay a minimum of $150.)

Some might add $21 billion thereto to compensate for dividends. They might then justify paying somewhere between $150 & $175 billion for Coca Cola. In the end such a price might not result poorly, but it is not what I consider very attractive either.

I think a reasonable price is $115 billion, though ideally it would be bought for $100 billion. As of Friday it was selling for about $105 billion. Such an inexpensive price for an outstanding company does not offer itself very often. I strongly suggest purchases of large quantities.

Purchasing Power, Investing, and why Index Funds do better than Mutual Funds

I have not the time to better organize this article nor to edit it fully, but it provides valuable information about fees and expenses of Mutual Funds, why they do not add anything to the investment management business, and how much they actually they take away from investors.

Click Below for Document:

Growing Purchasing Power & Mutual Funds Not the best Mix

Click Below for Document:

Growing Purchasing Power & Mutual Funds Not the best Mix

If to save, you MUST Invest (PART II INCOMPLETE)

Why you MUST invest

PART I

Consider you open a savings account and deposit $1000. You would obviously expect to have this money available for your use at a later date. Were you to return a year later to an account balance of $1000 you wouldn't likely think any thing of it. But imagine you went to withdraw your $1000 only to find $970. Now imagine the bank informs you (in all seriousness) that this was due to an imaginary tax. (I would love to witness your reactions.) Such a "tax" actually exists, its called inflation.

You're probably thinking that everyone knows about inflation, of course they do. But how much thought have you actually given it? If your answer is, "not much," don't feel bad, neither have most so called, "professionals" on Wall Street. I will try to put it into simple and relevant context.

Of course inflation has to do with rising prices of goods and services, though many people understandably tend to ignore it. Let me suggest two possible explanations: (i) Inflation is not clearly defined and (ii) incomes tend to go up at least slightly over time. Meaning, you might not immediately feel its effects in the same way as you might feel an income tax, but don't fool yourself, inflation is just as real.

To digress momentarily, let's look at the very basic concept of saving. The fundamental purpose to save rather than spend is to have more money in the future. In a simple world your savings grows simply by adding to it. (If you have $100 and add to it an additional $100, you now have $200, & $200 is obviously greater than $100. When most people save their money it is done with the thought that they will need it sometime in the future (e.g. to buy a house, for retirement, etc). The last thing anyone wants is to lose hard earned money, set aside for something specific and important.

You should try to understand that it is your money's ability to purchase goods and services that ultimately counts, and not the actual ("nominal") amount of dollar increases. I'll refer to this as "Purchasing power". If instead of buying a $1 coke today, you put the $1 into a saving account so that you can buy the coke on a later date. At that later date, you take the $1 and interest, if any, and go to the store to buy a coke. If upon purchase, you have change left over, your purchasing power can be said to have increased. If you have no change left over, your purchasing power can be considered maintained. If you can no longer afford the coke, your purchasing power can be said to have decreased.

Getting back to the inflation discussion, consider three savings accounts A, B, & C each with $1000. Where,

A - pays no interest

B - pays a fixed interest rate of 10%

C - pays a variable interest rate that fluctuates with the inflation rate

At the end of one year, account A would still have $1000, B would now have $1100, and if inflation were 3%, account C would have $1030:

A - (no interest) $1000

B - (@10%) $1100

C - (@3%) $1030

Since inflation was 3% for the year, goods and services would have increased also by 3%. Meaning an item that sold for $1000 at the beginning of the year, now sells for $1030.

The purchasing power of account A has decreased since a $1000 good or service last year now costs $1030 and your $1000 is $30 short.

Account B however increased its purchasing power by 10% or $100. The result is that at the end of the year this money could purchase the $1030 good or service, but $70 would be left over for use elsewhere.

The main point is that you are actually being taxed each year at the inflation rate if you hold money in a bank account that earns no interest. While this seems innocent enough let's take it a step further:

If you had $100,000 that earned no interest for 20 years, this is what you would see when you look at your account balance:

At the end of year 1, $100,000

At the end of year 2, $100,000

At the end of year 5, $100,000

At the end of year 10, $100,000

At the end of year 20, $100,000

Which is not so painful, until you go to spend it.

In real terms your purchasing power is reduced by the inflation rate, which we’ll assume is 3% for each year. Your equivalent balance in real terms:

At the end of year 1, $97,000

At the end of year 2, $94,090

At the end of year 5, $86,261

At the end of year 10, $74,409

At the end of year 20, $55,368

The cost of equivalent $100,000 goods due to inflation:

At the end of year 1, $103,030

At the end of year 2, $106,090

At the end of year 5, $115,927

At the end of year 10, $134,391

At the end of year 20, $180,611

You would have the exact same increase were you to earn 3% interest on $100,000:

At the end of year 1, $103,030

At the end of year 2, $106,090

At the end of year 5, $115,927

At the end of year 10, $134,391

At the end of year 20, $180,611

These relationships can be expressed in consistent terms more easily understood by taking the money you have in the bank, and dividing it by the cost of goods. To illustrate, if you have $100,000 and 3% inflation, a good that once cost $100,000 would in 20 years cost, $180,611:

100,000/180.611= .5573

Alternatively, if you think about it as a tax: A good costs $100,000 today & in 20 years, but you are taxed at 3%, then your balance is $55,368, 20 years hence:

55,368/100,000 = .5573

100,000/180,611 = .5573

55,683/100,000 = .5573

Meaning your purchasing power is 55.73% of what it once was.

Alternatively lets compare the situation in account C, the case that is able to earn a reasonable return (10%) above inflation (3%). The $100,000 account balance:

At the end of year 2, $121,000

At the end of year 5, $161,051

At the end of year 10, $259,374

At the end of year 20, $672,750

672,750/180,611 = 3.725

Meaning your purchasing power has substantially increased.

PART II (unfinished)

MAINTAINING PURCHASING POWER

It should be clear that in a world with inflation if your savings does not earn an average annual long-term interest rate that is at least equal to inflation, the value or purchasing power of your money is in decline even if the dollar amount is increasing.

If you are satisfied with simply maintaining your purchasing power, the best option is to put your money in Treasury Inflation-Protected Securities or “TIPS”. Government securities provide the safest means to preserve, but not increase purchasing power.

Since simply saving your money is not sufficient to maintain the initial amount saved, I will regard savings and investments as one in the same. The only way to earn interest on your money is to invest it. (If it is not clear why a thorough discussion is found further below.)

INCREASING PURCHASING POWER:

The most attractive avenue to grow your investments and purchasing power, and to guard against inflation is by investing in good American businesses. (While international businesses are also perfectly fine are not necessary for this conversation.) Most people do not have the means or the desire to invest their future purchasing power in private business and instead turn to public companies. This is arguably the better option anyway since if you don’t like the way things are going, it is easy to take your investment back and for most, there are many more to choose from. American businesses on average have in the last 20-30 years earned between 7-10 percent for investors and about 6-7 percent over a longer time frame, whereas inflation has averaged about 4% over the long term.

If you believe that in 20 years from now that our country’s standard of living will have risen, then the most sensible thing to do with your money is to own small pieces (stocks) of the best American Businesses (at sensible prices). The Standard of living can be measured by looking at income levels, quality of housing and food, medical care, educational opportunities, transportation, communications, etc. When economists talk about standard of living however, most are referring to changes in per capita (per person) Gross Domestic Product (GDP)-calculated by GDP divided by the population. GDP is defined as the total production of goods and services within the United States.

If the standard of living is thought to increase over time, then the GDP must also increase over time, meaning that the total production of goods and services must also increase accordingly and by definition the average business will march similarly upward. If you own a claim on a prosperous business, then by definition you must prosper too.

If your completely confused just think about it this way. Our country over the last century, has experienced two world wars, a great depression with unemployment of about 25%, two (possibly) three serious financial fiascos, the terrorist attacks of 9-11, the cold war, an assassinated president, the civil rights movement, etc. Yet our standard of living increased about seven-fold. Had you owned pieces of American businesses, you would have prospered similarly. There were however times that inflation rates were very high, even higher than most American businesses, and those who held cash or earned an unduly low return suffered significant long-term reductions in their future purchasing power.

Over the next century, it is certain that our country will experience periods of extreme uncertainty, but our country is equally certain to attain continued prosperity-a result of having a functional rule of law, belief in meritocracy, and an economic system that on the whole is market based.

[WILL ADD TO AND COMPLETE THIS SECTION SOON]!!!!!

PART I

Consider you open a savings account and deposit $1000. You would obviously expect to have this money available for your use at a later date. Were you to return a year later to an account balance of $1000 you wouldn't likely think any thing of it. But imagine you went to withdraw your $1000 only to find $970. Now imagine the bank informs you (in all seriousness) that this was due to an imaginary tax. (I would love to witness your reactions.) Such a "tax" actually exists, its called inflation.

You're probably thinking that everyone knows about inflation, of course they do. But how much thought have you actually given it? If your answer is, "not much," don't feel bad, neither have most so called, "professionals" on Wall Street. I will try to put it into simple and relevant context.

Of course inflation has to do with rising prices of goods and services, though many people understandably tend to ignore it. Let me suggest two possible explanations: (i) Inflation is not clearly defined and (ii) incomes tend to go up at least slightly over time. Meaning, you might not immediately feel its effects in the same way as you might feel an income tax, but don't fool yourself, inflation is just as real.

To digress momentarily, let's look at the very basic concept of saving. The fundamental purpose to save rather than spend is to have more money in the future. In a simple world your savings grows simply by adding to it. (If you have $100 and add to it an additional $100, you now have $200, & $200 is obviously greater than $100. When most people save their money it is done with the thought that they will need it sometime in the future (e.g. to buy a house, for retirement, etc). The last thing anyone wants is to lose hard earned money, set aside for something specific and important.

You should try to understand that it is your money's ability to purchase goods and services that ultimately counts, and not the actual ("nominal") amount of dollar increases. I'll refer to this as "Purchasing power". If instead of buying a $1 coke today, you put the $1 into a saving account so that you can buy the coke on a later date. At that later date, you take the $1 and interest, if any, and go to the store to buy a coke. If upon purchase, you have change left over, your purchasing power can be said to have increased. If you have no change left over, your purchasing power can be considered maintained. If you can no longer afford the coke, your purchasing power can be said to have decreased.

Getting back to the inflation discussion, consider three savings accounts A, B, & C each with $1000. Where,

A - pays no interest

B - pays a fixed interest rate of 10%

C - pays a variable interest rate that fluctuates with the inflation rate

At the end of one year, account A would still have $1000, B would now have $1100, and if inflation were 3%, account C would have $1030:

A - (no interest) $1000

B - (@10%) $1100

C - (@3%) $1030

Since inflation was 3% for the year, goods and services would have increased also by 3%. Meaning an item that sold for $1000 at the beginning of the year, now sells for $1030.

The purchasing power of account A has decreased since a $1000 good or service last year now costs $1030 and your $1000 is $30 short.

Account B however increased its purchasing power by 10% or $100. The result is that at the end of the year this money could purchase the $1030 good or service, but $70 would be left over for use elsewhere.

The main point is that you are actually being taxed each year at the inflation rate if you hold money in a bank account that earns no interest. While this seems innocent enough let's take it a step further:

If you had $100,000 that earned no interest for 20 years, this is what you would see when you look at your account balance:

At the end of year 1, $100,000

At the end of year 2, $100,000

At the end of year 5, $100,000

At the end of year 10, $100,000

At the end of year 20, $100,000

Which is not so painful, until you go to spend it.

In real terms your purchasing power is reduced by the inflation rate, which we’ll assume is 3% for each year. Your equivalent balance in real terms:

At the end of year 1, $97,000

At the end of year 2, $94,090

At the end of year 5, $86,261

At the end of year 10, $74,409

At the end of year 20, $55,368

The cost of equivalent $100,000 goods due to inflation:

At the end of year 1, $103,030

At the end of year 2, $106,090

At the end of year 5, $115,927

At the end of year 10, $134,391

At the end of year 20, $180,611

You would have the exact same increase were you to earn 3% interest on $100,000:

At the end of year 1, $103,030

At the end of year 2, $106,090

At the end of year 5, $115,927

At the end of year 10, $134,391

At the end of year 20, $180,611

These relationships can be expressed in consistent terms more easily understood by taking the money you have in the bank, and dividing it by the cost of goods. To illustrate, if you have $100,000 and 3% inflation, a good that once cost $100,000 would in 20 years cost, $180,611:

100,000/180.611= .5573

Alternatively, if you think about it as a tax: A good costs $100,000 today & in 20 years, but you are taxed at 3%, then your balance is $55,368, 20 years hence:

55,368/100,000 = .5573

100,000/180,611 = .5573

55,683/100,000 = .5573

Meaning your purchasing power is 55.73% of what it once was.

Alternatively lets compare the situation in account C, the case that is able to earn a reasonable return (10%) above inflation (3%). The $100,000 account balance:

At the end of year 2, $121,000

At the end of year 5, $161,051

At the end of year 10, $259,374

At the end of year 20, $672,750

672,750/180,611 = 3.725

Meaning your purchasing power has substantially increased.

PART II (unfinished)

MAINTAINING PURCHASING POWER

It should be clear that in a world with inflation if your savings does not earn an average annual long-term interest rate that is at least equal to inflation, the value or purchasing power of your money is in decline even if the dollar amount is increasing.

If you are satisfied with simply maintaining your purchasing power, the best option is to put your money in Treasury Inflation-Protected Securities or “TIPS”. Government securities provide the safest means to preserve, but not increase purchasing power.

Since simply saving your money is not sufficient to maintain the initial amount saved, I will regard savings and investments as one in the same. The only way to earn interest on your money is to invest it. (If it is not clear why a thorough discussion is found further below.)

INCREASING PURCHASING POWER:

The most attractive avenue to grow your investments and purchasing power, and to guard against inflation is by investing in good American businesses. (While international businesses are also perfectly fine are not necessary for this conversation.) Most people do not have the means or the desire to invest their future purchasing power in private business and instead turn to public companies. This is arguably the better option anyway since if you don’t like the way things are going, it is easy to take your investment back and for most, there are many more to choose from. American businesses on average have in the last 20-30 years earned between 7-10 percent for investors and about 6-7 percent over a longer time frame, whereas inflation has averaged about 4% over the long term.

If you believe that in 20 years from now that our country’s standard of living will have risen, then the most sensible thing to do with your money is to own small pieces (stocks) of the best American Businesses (at sensible prices). The Standard of living can be measured by looking at income levels, quality of housing and food, medical care, educational opportunities, transportation, communications, etc. When economists talk about standard of living however, most are referring to changes in per capita (per person) Gross Domestic Product (GDP)-calculated by GDP divided by the population. GDP is defined as the total production of goods and services within the United States.

If the standard of living is thought to increase over time, then the GDP must also increase over time, meaning that the total production of goods and services must also increase accordingly and by definition the average business will march similarly upward. If you own a claim on a prosperous business, then by definition you must prosper too.

If your completely confused just think about it this way. Our country over the last century, has experienced two world wars, a great depression with unemployment of about 25%, two (possibly) three serious financial fiascos, the terrorist attacks of 9-11, the cold war, an assassinated president, the civil rights movement, etc. Yet our standard of living increased about seven-fold. Had you owned pieces of American businesses, you would have prospered similarly. There were however times that inflation rates were very high, even higher than most American businesses, and those who held cash or earned an unduly low return suffered significant long-term reductions in their future purchasing power.

Over the next century, it is certain that our country will experience periods of extreme uncertainty, but our country is equally certain to attain continued prosperity-a result of having a functional rule of law, belief in meritocracy, and an economic system that on the whole is market based.

[WILL ADD TO AND COMPLETE THIS SECTION SOON]!!!!!

Lots of Capital = Less Attractive Returns

Ultimately the best investment managers will tend to have between $1-50 Billion under management or less (with long term average results of at least 15% after fees and expenses). That is because as you get beyond managing an amount greater than $50 Billion you have serious limitations insofar as your "investment universe" is concerned. To illustrate, say capital under management is indeed $50 Billion.

Lets assume two different managers, (i) and (ii). (i) owns 100 different companies and (ii) owns only 20-both are fully invested. With no other limitations (i) would be limited to businesses available for $500 million and above and (ii) limited to $2.5 Billion and above. But this is unrealistic since almost every fund of has some restriction as to the amount of ownership which can be established in any single business. Therefore assume limits of 25% and 5% ownership.

Now (i) is limited to

@25%, 500 Million x 4 = $2 Billion

@ 5%, 500 Million x 20 = $10 Billion

And (ii) limited to:

@25%, 2.5 Billion x 4 = $10 Billion

@ 5%, 2.5 Billion x 20 = $50 Billion

According to Morningstar, Total universe = 8831 stocks:

Businesses with market capitalizations greater than or equal to:

Market Cap.................. number of businesses

$ 0.5 Billion.................... 2666

$ 2.0 Billion..................... 1429

$ 2.5 Billion .................... 1291

$ 3.0 Billion ...................... 1137

$ 5.0 Billion ........................ 827

$10.0 Billion .....................526

$20.0 Billion ........................322

$50.0 Billion ......................131

Oh but now for a bit of reality. Lets make this realistic and say I am interested in only those funds that provide investors with long-term attractive rates of return or at least better returns than offered by an index fund after fees and expenses. So lets assume 10% as a better than average return, which it is or isn't depending on the period of years. Let's do a simple case, those businesses that meet the foregoing Market Cap restrictions, and earned 10% return on equity for the previous year (which I actually consider very average). This will obviously overstate the realistic number were we to look at only those with moderate amounts of leverage and who earned a 10 year return on equity at or above 10% and not just for a single year. At any rate:

The number of companies, Market Cap & 10%+ Return on equity

Market Cap................... number of businesses

$ 0.5 Billion................. 1651

$ 2.5 Billion.................. 950

$10.0 Billion................. 436

$50.0 Billion.................. 116

This is a long winded way of making the point that as you get above $50 Billion of investment Capital you quickly become restricted as to where one might intelligibly allocate investment capital. Oh, the number of businesses above $50 billion and earn at least 20% return on Equity (single year) amount to only 71 businesses, not removing therefrom those that are very highly leveraged.

A very, very limited list of such really, really great Investment Funds: (No Order)

Fund name, (State) Primary Manager

Fairholme (recently moved to Miami from NY) Bruce Berkowitz

Baupost Group (Boston) Seth Klarman

First Manhattan Consulting Group (NY) Sandy Gottesman

Gotham Capital (NY) Joel Greenblatt

Weiss Asset Management (Boston) Andrew Weiss

Tweedy Browne (New York) Christopher Browne

Chieftain Capital (NY) Glenn Greenburg

Longleaf Partners (Tennessee) Mason Hawkins

Semper Vic, under Gardner Russo & Gardner (PA) Tom Russo

Markel-Asset Management (Virginia) Thomas Gayner

H.L. Lichstrahl & Company (Virginia) Howard Lichstrahl

Lets assume two different managers, (i) and (ii). (i) owns 100 different companies and (ii) owns only 20-both are fully invested. With no other limitations (i) would be limited to businesses available for $500 million and above and (ii) limited to $2.5 Billion and above. But this is unrealistic since almost every fund of has some restriction as to the amount of ownership which can be established in any single business. Therefore assume limits of 25% and 5% ownership.

Now (i) is limited to

@25%, 500 Million x 4 = $2 Billion

@ 5%, 500 Million x 20 = $10 Billion

And (ii) limited to:

@25%, 2.5 Billion x 4 = $10 Billion

@ 5%, 2.5 Billion x 20 = $50 Billion

According to Morningstar, Total universe = 8831 stocks:

Businesses with market capitalizations greater than or equal to:

Market Cap.................. number of businesses

$ 0.5 Billion.................... 2666

$ 2.0 Billion..................... 1429

$ 2.5 Billion .................... 1291

$ 3.0 Billion ...................... 1137

$ 5.0 Billion ........................ 827

$10.0 Billion .....................526

$20.0 Billion ........................322

$50.0 Billion ......................131

Oh but now for a bit of reality. Lets make this realistic and say I am interested in only those funds that provide investors with long-term attractive rates of return or at least better returns than offered by an index fund after fees and expenses. So lets assume 10% as a better than average return, which it is or isn't depending on the period of years. Let's do a simple case, those businesses that meet the foregoing Market Cap restrictions, and earned 10% return on equity for the previous year (which I actually consider very average). This will obviously overstate the realistic number were we to look at only those with moderate amounts of leverage and who earned a 10 year return on equity at or above 10% and not just for a single year. At any rate:

The number of companies, Market Cap & 10%+ Return on equity

Market Cap................... number of businesses

$ 0.5 Billion................. 1651

$ 2.5 Billion.................. 950

$10.0 Billion................. 436

$50.0 Billion.................. 116

This is a long winded way of making the point that as you get above $50 Billion of investment Capital you quickly become restricted as to where one might intelligibly allocate investment capital. Oh, the number of businesses above $50 billion and earn at least 20% return on Equity (single year) amount to only 71 businesses, not removing therefrom those that are very highly leveraged.

A very, very limited list of such really, really great Investment Funds: (No Order)

Fund name, (State) Primary Manager

Fairholme (recently moved to Miami from NY) Bruce Berkowitz

Baupost Group (Boston) Seth Klarman

First Manhattan Consulting Group (NY) Sandy Gottesman

Gotham Capital (NY) Joel Greenblatt

Weiss Asset Management (Boston) Andrew Weiss

Tweedy Browne (New York) Christopher Browne

Chieftain Capital (NY) Glenn Greenburg

Longleaf Partners (Tennessee) Mason Hawkins

Semper Vic, under Gardner Russo & Gardner (PA) Tom Russo

Markel-Asset Management (Virginia) Thomas Gayner

H.L. Lichstrahl & Company (Virginia) Howard Lichstrahl

Better understanding of investments, Diversification, Books, The Economy...

Books:

You should be very careful what you read and who wrote it. You want to keep the noise to a minimum.

Read and re-read intelligent investor. May be boring but you need to understand what he says in that book.

Then go read The little book on value investing. By Christopher Browne. There is a lot of good additional material on his funds site, tweedybrowne.com

Before getting into Security Anaysis (1940 best to begin with) I would become familiar with what some accounting:

Tutorial on Financial Statements:

http://www.baruch.cuny.edu/tutorials/statements/

As you are learning try to think about the following: what is the company really earning and what can they expect to earn in the future? Also what do you reasonably not know?

Diversification?

Diversification is over used. The typical issue with investing in only a few businesses is that aggregate returns could be adversely affected by any one security. Investment selection should be based upon a thorough

understanding of each business and its underlying economics, acquired only at sensible prices. While seemingly obvious, the fact is that most people who buy fractional ownership do not know nearly what they should to make informed long-term investment decisions (the so called "professionals" included).

Ultimately, the premise is that it makes more sense to invest large amounts in those businesses with which you understand a great deal, instead of putting very small amounts in many business that you understand very little. Concentration may very well decrease risk if it raises, as it should, both the intensity with which an investor thinks about a business and the comfort-level he must feel with its economic characteristics before buying an ownership interest.

Some stuff to think about:

The fundamental purpose to save or invest versus spend is to have more money in the future. In a simple world, one without inflation or investments as alternatives to saving, the money grows through saving more out of income relative to what is consumed, or spent. Today’s dollars are valued in the same terms as are tomorrow’s dollars. Any interest earned on savings translates into increased purchasing power-the ability to buy something.

Introduce Inflation and money not spent must earn an amount equal to the inflation rate just to maintain purchasing power. This is because $1 today with 3% inflation means that you need $1.03 in a year from now in order to have the same "purchasing power". That is what costs $1 today costs $1.03 next year, so if you save (or invest) you must earn at least 3%, otherwise you have less money than you started with. If you are unable to earn 3% you should just spend the money.

In this world the fundamental problem is where to put money in order to grow future purchasing power. This implies a reasonable rate of return over inflation (ignoring income taxes for now).

On the Economy:

A few things on the economy and the "markets". Don't worry about what people say, friends, media, whoever. In the last 100 years we have had two world wars, a great depression where unemployment reached unbelievable levels, two almost three serious financial fiascos, 9-11, the cold war, an assassinated president, etc. yet our living standards increased seven-fold. So called "bad-times" lead to good investment opportunities because of depressed prices, but only those who didn't loose money are able to take advantage of this. I'll spare you, with more details. The moral being do not pay attention to discussions about interest rates, the economy, the stock market, etc. do what makes sense at all times, nothing less.

I hate thinking of business valuations like this but you may come across such terms and should be familiar with them:

Generally speaking, there are two very broad and contrasting ideas: a “macro” perspective as opposed to a "micro" perspective. A macro approach is often also called a “top down approach” whereas micro is bottom up. Basically the macro approach looks at things like sectors or industries, potential changes in interest rates, foreign exchange rates, and the like. For more information on the differences between top down and bottom up see the following link:

http://www.tiaa-cref.org/about/press/publications/market_monitor/2006_11_20.

pdf

It takes time and effort!

If investing were easy to do there would be many, many more people like Warren Buffet. And while there are many people that have made great fortunes in the investment management and related businesses nearly all of them made their money on fees not associated with actual investment results. So this is one reason not to pay attention to about 99% of these guys especially those on TV. Of the investors who actually invest in securities with successful long term “track records” nearly all of them might be referred to as Value Investors, with the exception of maybe one. George Soros is a successful investor who practices what seems to be a very much top down approach, but the problem is that he cannot explain his success although others will claim that they can. Some have written books about his approach, but if they truly understood it they would apply it by investing and not so much by writing books. (Same goes for all those books on Buffett.)

It is not my intent to undermine investors like Soros, but his approach or selection process is almost equivalent to throwing darts (at least as far as outsiders are concerned). For one, it is truly difficult to determine what

the ultimate factors were in their decision making process.

Assume one makes a decision to buy a given stock, the stock price goes up, and then the person decided to sell at a profit. Can it be said that a good investment decision has been made?

This has a very dangerous implication too often overlooked. Just because you made money on an investment doesn’t necessarily make it a good decision. If you invested in a housing company and a year later you sell making a 20% return on your investment you might conclude that indeed your choice was a good one in which case you are likely to make future investments based upon a similar thought process. But if the reason you decided to invest in that company was made based upon a belief that demand for new housing was to increase in the near term, but the company decided that demand for new houses was actually declining and in response they issued a regular dividend that appealed to the big mutual funds resulting in the biding up of the stock price.

Such would not qualify as a good investment decision in my mind, because the next investment

is not likely to result in such a positive outcome. That is, the next company you invest in may not have funds to distribute as a dividend and the price may very well then drop off significantly-the direct result of failing to account for price paid relative to reasonable business value.

"You are correct only because your decision was based on the facts and sound logic."

The Term Value Investing:

By the way The term Value investor is redundant. Value investing is considered purchasing businesses for less than they would sell to a knowledgeable buyer in a negotiated transaction. But this is the only form

of an "investment", otherwise you are speculating. Furthermore, the purchase of commons stocks must always be thought of as buying fractional ownership of the entire business. So think of "Value Investing" simply as "investing" and everything else as speculating. Speculating is the purchase of a "stock" on the basis that you believe the stock price will go up. Speculators in other words, DO NOT ask themselves (i) what exactly am I buying and (ii) is the price being offered an attractive one?

You should be very careful what you read and who wrote it. You want to keep the noise to a minimum.

Read and re-read intelligent investor. May be boring but you need to understand what he says in that book.

Then go read The little book on value investing. By Christopher Browne. There is a lot of good additional material on his funds site, tweedybrowne.com

Before getting into Security Anaysis (1940 best to begin with) I would become familiar with what some accounting:

Tutorial on Financial Statements:

http://www.baruch.cuny.edu/tutorials/statements/

As you are learning try to think about the following: what is the company really earning and what can they expect to earn in the future? Also what do you reasonably not know?

Diversification?

Diversification is over used. The typical issue with investing in only a few businesses is that aggregate returns could be adversely affected by any one security. Investment selection should be based upon a thorough

understanding of each business and its underlying economics, acquired only at sensible prices. While seemingly obvious, the fact is that most people who buy fractional ownership do not know nearly what they should to make informed long-term investment decisions (the so called "professionals" included).

Ultimately, the premise is that it makes more sense to invest large amounts in those businesses with which you understand a great deal, instead of putting very small amounts in many business that you understand very little. Concentration may very well decrease risk if it raises, as it should, both the intensity with which an investor thinks about a business and the comfort-level he must feel with its economic characteristics before buying an ownership interest.

Some stuff to think about:

The fundamental purpose to save or invest versus spend is to have more money in the future. In a simple world, one without inflation or investments as alternatives to saving, the money grows through saving more out of income relative to what is consumed, or spent. Today’s dollars are valued in the same terms as are tomorrow’s dollars. Any interest earned on savings translates into increased purchasing power-the ability to buy something.

Introduce Inflation and money not spent must earn an amount equal to the inflation rate just to maintain purchasing power. This is because $1 today with 3% inflation means that you need $1.03 in a year from now in order to have the same "purchasing power". That is what costs $1 today costs $1.03 next year, so if you save (or invest) you must earn at least 3%, otherwise you have less money than you started with. If you are unable to earn 3% you should just spend the money.

In this world the fundamental problem is where to put money in order to grow future purchasing power. This implies a reasonable rate of return over inflation (ignoring income taxes for now).

On the Economy:

A few things on the economy and the "markets". Don't worry about what people say, friends, media, whoever. In the last 100 years we have had two world wars, a great depression where unemployment reached unbelievable levels, two almost three serious financial fiascos, 9-11, the cold war, an assassinated president, etc. yet our living standards increased seven-fold. So called "bad-times" lead to good investment opportunities because of depressed prices, but only those who didn't loose money are able to take advantage of this. I'll spare you, with more details. The moral being do not pay attention to discussions about interest rates, the economy, the stock market, etc. do what makes sense at all times, nothing less.

I hate thinking of business valuations like this but you may come across such terms and should be familiar with them:

Generally speaking, there are two very broad and contrasting ideas: a “macro” perspective as opposed to a "micro" perspective. A macro approach is often also called a “top down approach” whereas micro is bottom up. Basically the macro approach looks at things like sectors or industries, potential changes in interest rates, foreign exchange rates, and the like. For more information on the differences between top down and bottom up see the following link:

http://www.tiaa-cref.org/about/press/publications/market_monitor/2006_11_20.

It takes time and effort!

If investing were easy to do there would be many, many more people like Warren Buffet. And while there are many people that have made great fortunes in the investment management and related businesses nearly all of them made their money on fees not associated with actual investment results. So this is one reason not to pay attention to about 99% of these guys especially those on TV. Of the investors who actually invest in securities with successful long term “track records” nearly all of them might be referred to as Value Investors, with the exception of maybe one. George Soros is a successful investor who practices what seems to be a very much top down approach, but the problem is that he cannot explain his success although others will claim that they can. Some have written books about his approach, but if they truly understood it they would apply it by investing and not so much by writing books. (Same goes for all those books on Buffett.)

It is not my intent to undermine investors like Soros, but his approach or selection process is almost equivalent to throwing darts (at least as far as outsiders are concerned). For one, it is truly difficult to determine what

the ultimate factors were in their decision making process.

Assume one makes a decision to buy a given stock, the stock price goes up, and then the person decided to sell at a profit. Can it be said that a good investment decision has been made?

This has a very dangerous implication too often overlooked. Just because you made money on an investment doesn’t necessarily make it a good decision. If you invested in a housing company and a year later you sell making a 20% return on your investment you might conclude that indeed your choice was a good one in which case you are likely to make future investments based upon a similar thought process. But if the reason you decided to invest in that company was made based upon a belief that demand for new housing was to increase in the near term, but the company decided that demand for new houses was actually declining and in response they issued a regular dividend that appealed to the big mutual funds resulting in the biding up of the stock price.

Such would not qualify as a good investment decision in my mind, because the next investment

is not likely to result in such a positive outcome. That is, the next company you invest in may not have funds to distribute as a dividend and the price may very well then drop off significantly-the direct result of failing to account for price paid relative to reasonable business value.

"You are correct only because your decision was based on the facts and sound logic."

The Term Value Investing:

By the way The term Value investor is redundant. Value investing is considered purchasing businesses for less than they would sell to a knowledgeable buyer in a negotiated transaction. But this is the only form

of an "investment", otherwise you are speculating. Furthermore, the purchase of commons stocks must always be thought of as buying fractional ownership of the entire business. So think of "Value Investing" simply as "investing" and everything else as speculating. Speculating is the purchase of a "stock" on the basis that you believe the stock price will go up. Speculators in other words, DO NOT ask themselves (i) what exactly am I buying and (ii) is the price being offered an attractive one?

Follow up:

My friend has Pioneer. They are worse.

I told him that his returns were 80% of the returns Pioneer claims to earn.

He asked, "So are you saying that Pioneer's fees are 20%"?

My Response:

No, well not really: Industry standard is that charges are a % of assets, but they can increase assets more and more as people give them money through 401k's etc. The other factor is the "load" either front-end or back, both are bad. What matters to you however is how much of the money that you "earned" (the amount in excess of the amount that you directly put in), will you actually be able to take away. In other words there is what they call a "total return", (what the fund claims to have "earned" you) and then there is the amount that you can put in the bank at the time of sale called redemption (excluding income taxes). The amount (again pre-tax) you can put in the bank is much less than the "total return". It is actually the total return less fees and expenses.

Therefore in response to, "So are you saying that pioneer's fees are 20%," the answer is no but yes. Technically they charge you something like 0.7% per year in expenses in combination with the front-load fee (4.5%? Or whatever it was) actually reduce the "total return" by 20%. So the answer is also yes your take-away return is actually 0.80 or 80% of the "total return".

Maybe an example:

You put in $10,000 and for ease, assume you never add to it. With the front load (say of 4.5%) you actually begin not with $10,000, but with $9550 because:

95.5% = (100% - 4.5%) and .955 x $10000 = 9550.

And from then on you are expensed each year at some seemingly marginal rate, but that is in essence cumulative and takes away from your take away returns as well.

So Lets assume they report to you that they earned 10% and they do this each year for 20 years. Your $10,000 should now be $67,275, which of course is an annual return of 10%.

This is a simple calculation which you could do with a constant rate of return, its just 10,000 x 1.10^20 (note ^20 is "to the 20th power")

So they can claim to have earned you 10%, but wait a minute, you began, not with $10,000, but with $9550 due to the front end load, which at 10% for 20 years would be $64,247.62

Yet there is still more since each year they are deducting the annual expense from your balance. So if for each year your funds go up by 10%, the 10% is immediately reduced by say 0.7% or 0.007. This may seem like a small number but over time this "frictional" cost is significant.

The end result is that they may claim to have earned you 10% annually, but after calculating the cumulative frictional costs and reducing the beginning balance by the front load fee, 10% is actually 10% x (1-.20) or 10% x .80 = 8%.

The result, the take away dollar amount (pre tax) from your $10,000 investment would be 46,609.57 not $67,275. Big difference! Oh and by the way, these funds WILL NOT EARN 10% ANYWAY and will be lucky to earn 8% before these expenses, but that is another discussion altogether.

My friend has Pioneer. They are worse.

I told him that his returns were 80% of the returns Pioneer claims to earn.

He asked, "So are you saying that Pioneer's fees are 20%"?

My Response:

No, well not really: Industry standard is that charges are a % of assets, but they can increase assets more and more as people give them money through 401k's etc. The other factor is the "load" either front-end or back, both are bad. What matters to you however is how much of the money that you "earned" (the amount in excess of the amount that you directly put in), will you actually be able to take away. In other words there is what they call a "total return", (what the fund claims to have "earned" you) and then there is the amount that you can put in the bank at the time of sale called redemption (excluding income taxes). The amount (again pre-tax) you can put in the bank is much less than the "total return". It is actually the total return less fees and expenses.

Therefore in response to, "So are you saying that pioneer's fees are 20%," the answer is no but yes. Technically they charge you something like 0.7% per year in expenses in combination with the front-load fee (4.5%? Or whatever it was) actually reduce the "total return" by 20%. So the answer is also yes your take-away return is actually 0.80 or 80% of the "total return".

Maybe an example:

You put in $10,000 and for ease, assume you never add to it. With the front load (say of 4.5%) you actually begin not with $10,000, but with $9550 because:

95.5% = (100% - 4.5%) and .955 x $10000 = 9550.

And from then on you are expensed each year at some seemingly marginal rate, but that is in essence cumulative and takes away from your take away returns as well.

So Lets assume they report to you that they earned 10% and they do this each year for 20 years. Your $10,000 should now be $67,275, which of course is an annual return of 10%.

This is a simple calculation which you could do with a constant rate of return, its just 10,000 x 1.10^20 (note ^20 is "to the 20th power")

So they can claim to have earned you 10%, but wait a minute, you began, not with $10,000, but with $9550 due to the front end load, which at 10% for 20 years would be $64,247.62

Yet there is still more since each year they are deducting the annual expense from your balance. So if for each year your funds go up by 10%, the 10% is immediately reduced by say 0.7% or 0.007. This may seem like a small number but over time this "frictional" cost is significant.

The end result is that they may claim to have earned you 10% annually, but after calculating the cumulative frictional costs and reducing the beginning balance by the front load fee, 10% is actually 10% x (1-.20) or 10% x .80 = 8%.

The result, the take away dollar amount (pre tax) from your $10,000 investment would be 46,609.57 not $67,275. Big difference! Oh and by the way, these funds WILL NOT EARN 10% ANYWAY and will be lucky to earn 8% before these expenses, but that is another discussion altogether.

Why Mutual Funds are not really the best option

American Funds :

Assets under Management, 1.4 Trillion Dollars no wonder the aggregate returns are only average. Incentives are to accumulate investor funds, not to earn investors money.

Assets under Management, 1.4 Trillion Dollars no wonder the aggregate returns are only average. Incentives are to accumulate investor funds, not to earn investors money.

I am dumbfounded as to why people continue to fund institutions that provide significantly less than an index return. It is just crazy to me that (for example) American Funds with 1.4 Trillion Dollars under management, boast to investors an (aggregate) compounded annual return over the last 5 and 10 year periods of 10% and 6.9% respectively. Although only very average, is unfortunately very much overstated. After consideration of fees and expenses, these 5 & 10 year returns would be reduced to 8.14% and 5.5% respectively and that is before income (capital gains) tax. Furthermore they may claim a 12% return to investors since inception (56 years) which after fees and expenses turns out to be 8.76% versus a return for the for the S&P 500 of 11.1%. -Makes no sense to me-

{kind=link}

Assets under Management, 1.4 Trillion Dollars no wonder the aggregate returns are only average. Incentives are to accumulate investor funds, not to earn investors money.

Assets under Management, 1.4 Trillion Dollars no wonder the aggregate returns are only average. Incentives are to accumulate investor funds, not to earn investors money.I am dumbfounded as to why people continue to fund institutions that provide significantly less than an index return. It is just crazy to me that (for example) American Funds with 1.4 Trillion Dollars under management, boast to investors an (aggregate) compounded annual return over the last 5 and 10 year periods of 10% and 6.9% respectively. Although only very average, is unfortunately very much overstated. After consideration of fees and expenses, these 5 & 10 year returns would be reduced to 8.14% and 5.5% respectively and that is before income (capital gains) tax. Furthermore they may claim a 12% return to investors since inception (56 years) which after fees and expenses turns out to be 8.76% versus a return for the for the S&P 500 of 11.1%. -Makes no sense to me-

Subscribe to:

Posts (Atom)